If you haven’t been paying attention to Blockchain – now is the time to start!

Over the years, the uses for blockchain have grown significantly. What does it mean for businesses and startups

Over the years, the uses for blockchain have grown significantly. Blockchain technology has become mainstream, with more and more companies taking advantage of the benefits it offers. Businesses and startups should make sure they are making the most of blockchain technology. Meanwhile, professionals can enhance their understanding of blockchain to have their future businesses harness its use cases.

A refresher on blockchain

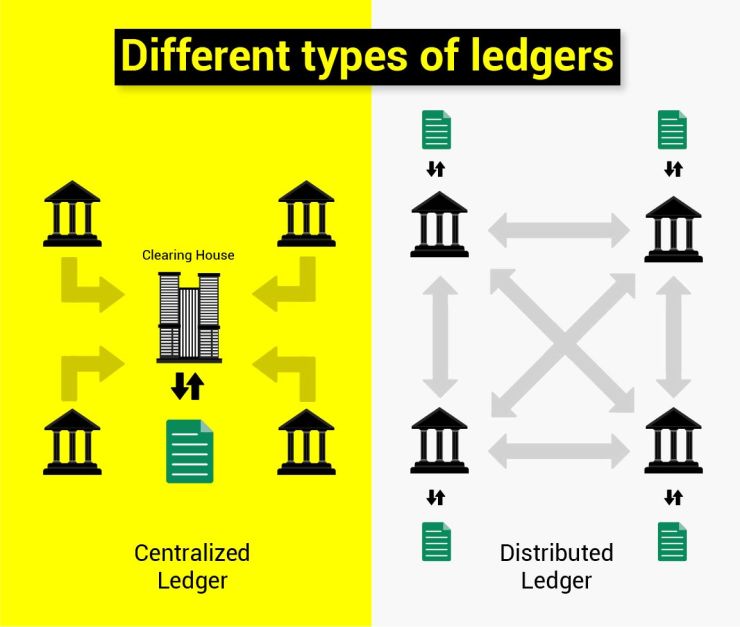

Blockchain is a distributed ledger. Think of it as a structure that lets us store transactional records in the form of blocks. The “chain” aspect of the term “blockchain” comes from the combination of multiple databases that support blockchain, working together to form a network. This is a digital ledger.

All transactions within the blockchain’s ledger have digital signatures. This means that while anyone can freely view the information within the blockchain, they cannot change the information. That, in turn, delivers security.

That high level of security is one of the reasons that blockchain technology is so popular. Its decentralized nature is another, as you do not have to rely on a central authority or government. The ability to program blockchain with smart contracts and other pieces of code also allow for the convenience of automatic payments, events, and more.

How many transactions rely on blockchain?

In its early years, blockchain technology was primarily used in cryptocurrencies or in projects that were somehow related to the crypto space. That has changed over the years. There is an increasing number of projects and companies outside of the crypto world taking advantage of blockchain.

Data from Blockchain.com shows that the number of total blockchain transactions has been steadily increasing throughout its history. It is now at nearly 640 million transactions as of April 2021. Bitcoin alone averages about 250,000 to 300,000 transactions per day in the last few months.

To put the extent of blockchain adoption into perspective, consider that experts predict global spending on blockchain solutions will reach $11.7 billion by 2022. The market for blockchain technology will gain an estimated $20 billion in revenues by 2024.

Predictions regarding the future of blockchain adoption show its importance outside of crypto. By the time 2020 came to an end, 60% of CIOs were close to integrating blockchain. Also, in 2020, 20% of Internet of Things technologies featured blockchain-related services. Experts predict that by 2025, 55% of the health care applications will be using blockchain commercially.

Blockchain also has significant potential for the banking and financial industries. Using blockchain can reduce infrastructure costs for banks by up to 30% and save financial companies as much as $12 billion annually. With that in mind, it makes sense that the financial sector makes up 46% of the investments in blockchain technology. Other sectors with high investments include manufacturing accounting for 12%, energy utilities with another 12%, health care with 11%, government with 8%, retail with 4%, and entertainment and media with 1%.

Learn how to develop the most in-demand skills for your future career!

Discover how you can acquire the most in-demand skills with our free report, and open the doors to a successful career.

Why should businesses learn more about blockchain?

Businesses should take the time to learn about blockchain and its various use cases because of the numerous applications that this technology has. Put simply, blockchain offers numerous opportunities for businesses to overcome challenges, as well as opportunities to take advantage of opportunities.

Creating contracts and contract accountability

Contracts are an important part of any business interaction. However, creating them is time-consuming and expensive. They can also frequently be hard to enforce.

Smart contracts on the blockchain make it significantly easier to create contracts with just a few lines of code. There are no concerns about following through with the contract as smart contracts will execute the outlined actions automatically when an agreed-upon condition occurs. There is also no chance to manipulate the contract, as smart contracts are on the blockchain and therefore immutable.

Cross-border payments

Cross-border payments are important for any modern business, as more people are working with international customers. However, international payments are time-consuming and have high fees.

Blockchain eliminates or dramatically reduces those fees and can deliver near-instant payments that take a matter of seconds. This is possible, thanks to the distributed ledger and the immutability of transactions. One estimate from Deloitte says that using blockchain reduces remittance fees by 40-80%.

Crowdfunding or non-profit fundraising

The blockchain also offers solutions for crowdfunding, with or without the use of cryptocurrencies or tokens. The major concerns with commonly-used crowdfunding methods are transparency, security, and investor abuse.

The blockchain can streamline the process and provide transparency to ensure that the raised funds will be used as intended.

Capital markets

Businesses in the finance world can use the blockchain to improve the capital markets. Perhaps the biggest benefit would be the quick transaction times, which will result in faster settlement and clearing.

Another big benefit would be the immutability of the ledger and its detailed records. That leads to a convenient audit trail all in one place.

Digital piracy and copyright

With the prevalence of the internet and streaming platforms, there is a big issue with digital piracy that takes away profits from creators and owners of the content.

The NFT, which we’ll discuss in more detail, is one way to resolve this issue, but blockchain also offers other options. For example, blockchain can let creators digitize intellectual property rights and other metadata in the immutable ledger. The blockchain can also show all of the times the content was accessed, making it easier to catch digital pirates.

Healthcare patient data

In health care, one of the major challenges is handling the large volume of patient data. It needs to be accessible to various members of the medical team but only to authorized users. The current system has issues dealing with those challenges and finding a convenient way for medical providers to share patient information with each other when needed.

Companies can use blockchain to create decentralized databases of patient data that hospitals can access with the appropriate permission. One option for ensuring privacy is to use secure codes instead of identities or a private key.

Identity theft

Identity theft is more of a concern for individuals than businesses. However, it is still relevant, especially when businesses or governments rely on identification.

Thanks to the fact that blockchain features both private and public keys, it helps prevent this issue. The public key is available to everyone, while only you have the private key. Blockchain programs can require the private key to adjust information or share the most private bits of information, such as your social security number. At the same time, the public key can be used to confirm your identity.

Marketing

Blockchain can help marketers get more data regarding consumer behavior and client information. Specifically, it can help them keep that data organized and ensure its accuracy.

The blockchain can also let marketing teams confirm when something changed in the marketing campaign.

It can even help confirm that traffic is from a real person instead of a bot.

Real estate

Blockchain technology also has potential use cases in real estate. It can help overcome challenges related to intermediaries and background checks.

One of the biggest use cases is the ability to use blockchain to prove property ownership. The immutability of the ledger comes into play here, as no one can alter the ledger. Meanwhile, smart contracts can remove the need to use intermediaries or escrow services, saving time and money.

Regulatory compliance

Any type of business that has to comply with regulations can use blockchain to help prove that compliance. The transparency and immutability of the ledger come in handy here. Furthermore, it is harder for regulators to accuse companies of fraud with blockchain as the ledger is immutable.

Supply chain management

Supply chain management is another complicated issue that businesses face, and blockchain technology can make it easier. Supply chains tend to be disconnected and come with a risk of fraud, along with high overhead costs. All members of the supply chain need to be on the same page, but this is not always possible.

Blockchain resolves this issue, thanks to its transparency and the fact that the information is available to everyone, yet no one can change it. This lets vendors, manufacturers, and everyone else in the supply chain view the same information.

The real-time tracking capability of blockchain also reduces the risk of misplaced items.

Opportunity: NFTs

One of the many opportunities that come from blockchain is the NFT or non-fungible token. Each NFT is unique. This means that two NFTs of the same type cannot be traded for each other and be used equally. That contrasts with how you could exchange a dollar for another dollar or a Bitcoin for a Bitcoin without any differences. They use the Ethereum blockchain.

NFTs present opportunities for digital art, music, and other creative items. The most popular application is using NFTs for a digital variation of collecting fine art. Still, there are also other potential applications that businesses in the creative industries should look into. This is true given that you can set up NFTs so that the creator (your business) receives a percentage of the profits for every resale of the creative item.

Exploring opportunities for startups worldwide to leverage blockchain

Many of the opportunities for startups to leverage blockchain overlap with the ways that blockchain can overcome the previously mentioned business challenges.

For example, a startup could create an identity verification system or design a patient database system for health care. One could create a system of supply chain management using blockchain. The possibilities are limitless with some creativity. Startups could also use blockchain to source funding via crowdfunding.

Using blockchain for transactions will also let startups monitor transactions and reduce fees. The latter is particularly important for a startup company on a tight budget.

BitClout

BitClout is a great example of how startups can get creative and find a unique service to offer that uses blockchain. In the case of BitClout, it is “the crypto social network.” BitClout is a proof-of-work blockchain that anonymous developers created to run a new type of social media. It has social tokens representing real people, and automated market makers control the supply of those social tokens. Before using the platform, you need to buy BTCLT. The only caveat is that so far, you cannot convert those tokens back.

The following are some of the other opportunities for startups to leverage blockchain technology.

Esports and traditional sports

Savvy startups could use blockchain to create loyalty programs, tokenize teams, and expand the markets for profit from esports and sports. Or they can develop a blockchain-based system to track engagement levels.

Improve business processes

Startups can use blockchain to streamline their business processes from the start instead of having to incorporate them later like an existing business would. For example, blockchain can streamline accounting (via transactions, including cross-border ones) and the supply chain.

Strengthen security

Startups tend to be more vulnerable to cybercriminals because of their lower marketing budgets. The blockchain reduces these concerns as you can track events and safely share data.

Are you ready to take your career to the next level?

Nexford's Career Path Planner takes into account your experience and interests to provide you with a customized roadmap to success.

Receive personalized advice on the skills and qualifications you need to get ahead in areas like finance, marketing, management and entrepreneurship.

How Ethereum fits into blockchain?

Ethereum is a blockchain created to help run decentralized applications and provide smart contracts. It is the basis for many blockchain solutions, as it was developed to support decentralized apps instead of requiring developers to start from scratch.

What Ethereum already powers

To show how important Ethereum is, consider some of the big names that already use it to incorporate blockchain technology.

Amazon added the Ethereum platform to the plans for the Amazon Managed Blockchain, which it will officially join with the summer update. This is crucial as Amazon Managed Blockchain prevents companies from having to develop their own blockchain. As such, this move makes Ethereum even more accessible to other businesses.

Microsoft is also using Ethereum, building its cloud storage platform Azure on it. This will expand Microsoft’s offerings to include more Ethereum-based solutions. Another use case example is Starbucks’ plan to use it to track its coffee’s lifecycle from the plant all the way to the cup.

Meanwhile, JPMorgan decided to launch its own cryptocurrency and to do so using Ethereum. The result is Quorum, is an enterprise-focused Ethereum platform created to take care of the bank’s back-office tasks. The same company is also the first big name to develop a digital coin for US Dollars. JPMorgan now has the JPM Coin to speed up payments and power the platform.

Ubisoft, the video game publisher, is building on Ethereum with its Rabbids Token, which is part of a game. The company also backs blockchain startups.

In the financial sector, the Dutch bank ING has been working on Ethereum since 2017. It has several projects, including the bilateral credit letter Bamboo, payment settlement consortium Fnality, and Kmogo for streamlining trading documents.

Another financial example comes from TD Ameritrade, which invested in ErisX. This is a regulated spot exchange that relies on smart contracts to streamline trades.

Why is Ethereum traded as a cryptocurrency?

Ethereum is also traded as a cryptocurrency in the form of ETH (technically known as Ether). Ether exists to pay for the computing power required to power the Ethereum blockchain. Ethereum’s developers consider Ether as fuel or gas for apps to work on the network. Essentially, Ether, or the cryptocurrency form of Ethereum, is necessary to power the network. Because that cryptocurrency has many use cases, people decided to invest in it as a currency as well.

Businesses of any size and type should be considering embracing blockchain to reap the benefits in terms of security, transactions, and overcoming current challenges.

Want to learn more about blockchain? Discover our MBA Specialization with Enabling E-Commerce and Digital Strategy. We also offer an MBA in Fintech and Blockchain.

Fadl is Founder & CEO of Nexford University. His vision is to enable greater social and economic mobility through high-quality, affordable education.

Join our newsletter and be the first to receive news about our programs, events and articles.